سنجش وضعیت شاخصهای مستندسازی حسابرسی با بهکارگیری تکنولوژیهای مبتنی بر اینترنت

کلمات کلیدی:

مستندسازی حسابرسی, تکنولوژیهای مبتنی بر اینترنت, داده های بزرگ مقیاس, فناوری اطلاعات, کیفیت حسابرسیچکیده

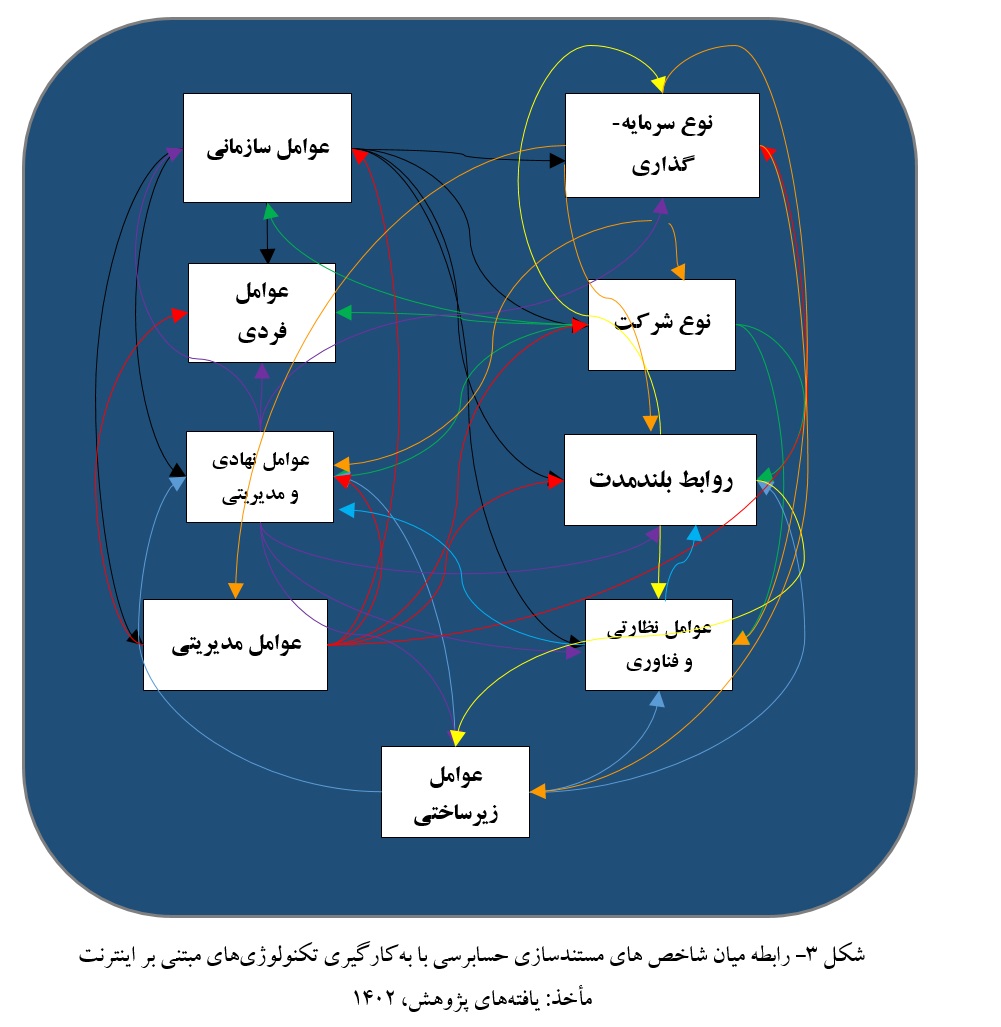

در حال حاضر کمبود یک مدل جامع در رابطه با کاربرد تکنولوژیهای مبتنی بر اینترنت در شکلگیری کار حسابرسان به وضوح احساس میشود. در واقع مساله اصلی این تحقیق، لزوم وجود یک نگاه همهجانبه به کاربردهای بالقوه فناوریهای مبتنی بر اینترنت بر شکلگیری کار حسابرسان است؛ چرا که در اغلب تحقیقات پیشین تنها به اثبات این قضیه پرداخته شده است که فناوریهای دیجیتال تاثیر مثبتی بر عملکرد حسابرسی دارند و مسائلی همچون عوامل زمینهای، عوامل مداخلهگر و استراتژیهای لازم برای پیادهسازی فناوریهای دیجیتال در حوزه حسابرسی کمتر مورد توجه قرار گرفته است. هدف از پژوهش حاضر سنجش وضعیت شاخصهای مستندسازی حسابرسی با بهکارگیری تکنولوژیهای مبتنی بر اینترنت میباشد. پژوهش حاضر به لحاظ روش، توصیفی – تحلیلی و به لحاظ هدف کاربردی میباشد. برای تحلیل دادهها از تکنیکهای دیمتل فازی و ANP فازی استفاده شده است. نتایج حاصل از دیمتل فازی نشان داده است که میزان تأثیرگذاری شاخص "عوامل سازمانی" بر مستندسازی حسابرسی با بهکارگیری تکنولوژیهای مبتنی بر اینترنت نسبت به سایر شاخصها بیشتر میباشد و شاخص "عوامل مدیریتی" در اولویت بعدی قرار دارد. همچنین میزان تأثیرپذیری شاخص "عوامل نظارتی و فناوری" نیز از سایر شاخصها بیشتر میباشد. همچنین نتایج حاصل از ANP فازی نشان داده است که شاخص عوامل سازمانی در اولویت اول و شاخص روابط بلندمدت در اولویت دوم و بقیه شاخصها در اولویت سوم قرار گرفتهاند.

دانلودها

مراجع

Auditing Standard, A. (2007). Documentation, Revised 2007: Effective for auditing financial statements for financial

periods starting from April 1, 2007, and thereafter.

Delbari Raghb, M., & Ismailzadeh Moghri, A. (2023). Independent Audit Quality Model Emphasizing Stakeholder

Needs. Financial Accounting and Auditing Research, 15(1), 69-98. https://acctgrev.ut.ac.ir/article_88664.html

Gonçalves, M. J. A., da Silva, A. C. F., & Ferreira, C. G. (2022). The Future of Accounting: How Will Digital

Transformation Impact the Sector? Informatics, 9(1), 19. https://doi.org/10.3390/informatics9010019

Guşe, G. R., & Mangiuc, M. D. (2022). Digital Transformation in Romanian Accounting Practice and Education: Impact

and Perspectives. Amfiteatru Economic, 24(59), 252-267. https://doi.org/10.24818/EA/2022/59/252

Hosseian Kashani, Z., Hajihasani, Z., Jahangirnia, H., & Gholami Jamkarani, R. (2021). Developing an Auditing

Documentation Quality Model Based on Grounded Theory Approach. Quarterly Journal of Financial Accounting

Research and Auditing, 13(52), 151-184. https://www.sid.ir/fa/Journal/ViewPaper.aspx?ID=578002

Izzo, M. F., Fasan, M., & Tiscini, R. (2021). The Role of Digital Transformation in Enabling Continuous Accounting

and the Effects on Intellectual Capital: The Case of Oracle. Meditari Accountancy Research.

https://doi.org/10.1108/MEDAR-02-2021-1212

Kamali Dolatabadi, M., & Darabi, R. (2022). The Role of Accounting Information Systems in Management and Cost

Reduction. Future Studies and Policy-Making, 8(26), 134-162. https://civilica.com/doc/1703907/

Pandey, N., Nayal, P., & Rathore, A. S. (2020). Digital Marketing for B2B Organizations: Structured Literature Review

and Future Research Directions. Journal of Business & Industrial Marketing. https://doi.org/10.1108/JBIM-06-

-0283

Sabuncu, B. (2022). The Effects of Digital Transformation on the Accounting Profession. Ömer Halisdemir Üniversitesi

İktisadi Ve İdari Bilimler Fakültesi Dergisi, 15(1), 103-115. https://doi.org/10.25287/ohuiibf.974840

Saghafi, A., & Jamalianpour, M. (2018). Technology, Blockchain, and the Future of Accounting and Auditing.

Accountant Journal, 34(2), 9-15. https://hesabdar.iica.ir/files/pdf/1397/3/hesabdar-1397-3-314-9-15.pdf

Sandner, P., Lange, A., & Schulden, P. (2020). The Role of the CFO of an Industrial Company: An Analysis of the

Impact of Blockchain Technology. Future Internet, 12(8), 128. https://doi.org/10.3390/fi12080128

Stafie, G., & Grosu, V. (2022). Digital Transformation of Accounting as a Result of the Implementation of Artificial

Intelligence in Accounting. Romanian Journal of Economics, 54(1 (63)), 95-112.

https://journals.indexcopernicus.com/publication/4025478

Yigitbasioglu, O., Green, P., & Cheung, M. Y. D. (2022). Digital Transformation and Accountants as Advisors.

Accounting, Auditing & Accountability Journal. https://doi.org/10.1108/AAAJ-02-2019-3894

Ziyadin, S., Suieubayeva, S., & Utegenova, A. (2019). Digital Transformation in Business. International Scientific

Conference "Digital Transformation of the Economy: Challenges, Trends, New Opportunities",

چاپ شده

ارسال

بازنگری

پذیرش

شماره

نوع مقاله

مجوز

حق نشر 2024 تکنولوژی در کارآفرینی و مدیریت استراتژیک

این پروژه تحت مجوز بین المللی Creative Commons Attribution-NonCommercial 4.0 می باشد.