ارائه الگوی رویکردی نو در مدیریت استراتژیک سازمانها با تأکید بر حسابداری زیستمحیطی مبتنی بر شاخصهای مسئولیت اجتماعی و کیفیت حسابرسی

کلمات کلیدی:

مدیریت استراتژیک, حسابداری زیستمحیطی, مسئولیت اجتماعی, کیفیت حسابرسیچکیده

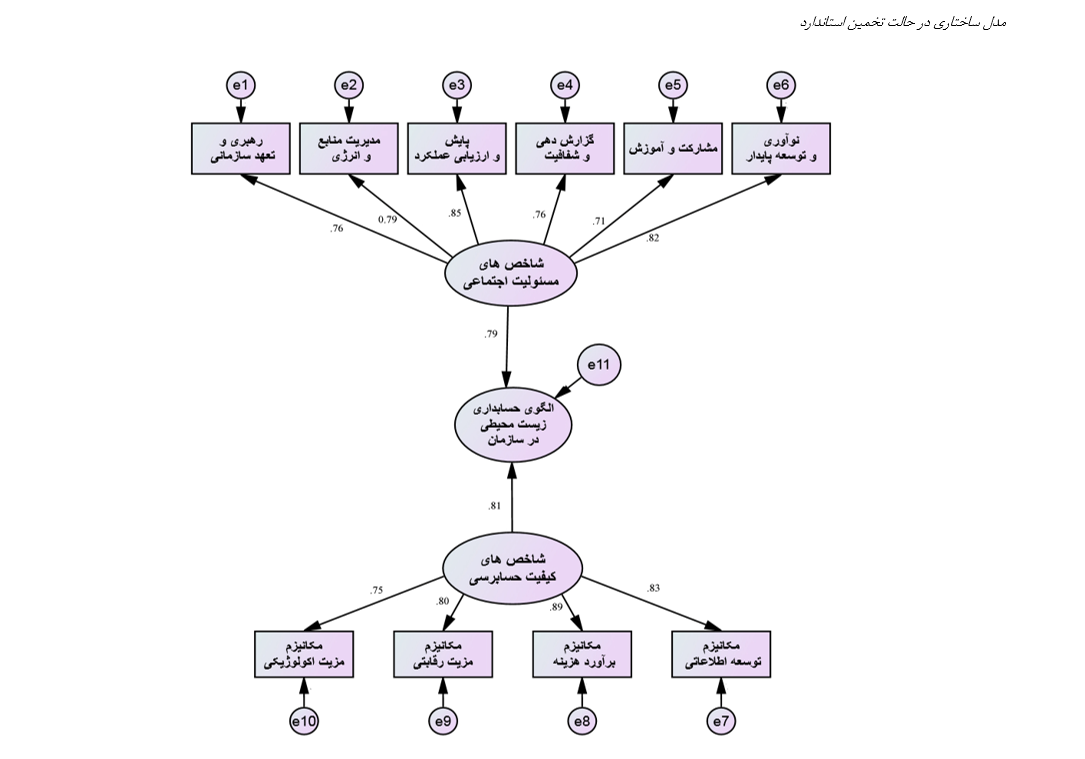

حسابداری زیستمحیطی بهعنوان ابزاری برای ثبت و گزارشگیری از فعالیتهای زیستمحیطی سازمان، به افزایش شفافیت و پاسخگویی کمک میکند و درعینحال، سازمانها را به سمت پایداری هدایت میکند. این تحقیق با هدف بررسی رابطه میان حسابداری زیستمحیطی، مسئولیت اجتماعی و کیفیت حسابرسی، در پی ارائه مدلی است که بتواند به سازمانها در بهبود شفافیت، پایداری و تعهد به مسئولیتهای اجتماعی کمک کند. روش تحقیق پژوهش حاضر به شیوه آمیخته کیفی- کمی بود. در بخش کیفی جامعه آماری شامل خبرگان آشنا به موضوع پژوهش (اساتید دانشگاه در حوزه مورد مطالعه) بود که نمونهگیری در این بخش پژوهش بهطور نظری انجام گرفت و در بخش کمی جامعه آماری شامل مدیران مالی شرکت های بورس و اوراق بهادار تهران بود که تعداد 119 نفر به استفاده از نمونه گیری در دسترس به عنوان نمونه اماری در نظر گرفته شدند. روش تجزیهوتحلیل اطلاعات در بخش کیفی بر اساس کدگذاری باز و محوری و در بخش کمی از آزمون kmo و بارتلت، آزمون تی تک نمونهای در نرمافزار SPSS و معادلات ساختاری در نرمافزار AMOS استفاده شده است. نتایج این مطالعه نشان میدهد که حسابداری زیستمحیطی میتواند نقش مهمی در بهبود مسئولیتپذیری اجتماعی سازمانها و ارتقای کیفیت حسابرسی داشته باشد و بهطورکلی میتوان بیان کرد که این مدل کاربردی میتواند بهعنوان یک ابزار راهبردی در بهبود عملکرد زیستمحیطی و اجتماعی سازمانها مورد استفاده قرار گیرد و نتایج مثبت آن به استحکام و پایداری روابط سازمانی و بهبود کیفیت حسابرسی منجر شود.

دانلودها

مراجع

Abed, I. A., Hussin, N., Haddad, H., Al-Ramahi, N. M., & Ali, M. A. (2022). The moderating effects of corporate social responsibility on the relationship between creative accounting determinants and financial reporting quality. Sustainability, 14(3), 1195. https://doi.org/10.3390/su14031195

Agnes, K. (2023). The effect of green accounting, company size, profitability, media disclosure, and board of commissioners' size on corporate social responsibility disclosure. International Journal Papier Public Review, 4(2), 1-17. https://doi.org/10.47667/ijppr.v4i2.203

Ahmed, Z., Asghar, M. M., Malik, M. N., & Nawaz, K. (2020). Moving towards a sustainable environment: the dynamic linkage between natural resources, human capital, urbanization, economic growth, and ecological footprint in China. Resources Policy, 67, 101677. https://doi.org/10.1016/j.resourpol.2020.101677

Akbar, N. B. A., & Mahdi, F. S. (2023). The Interest of the Supreme Audit Institution in Sustainable Economic, Social and Environmental Development on the Audit Quality Performance. International Journal of Professional Business Review, 8(1), 21. https://doi.org/10.26668/businessreview/2023.v8i1.1164

Al-Shaer, H. (2020). Sustainability reporting quality and post-audit financial reporting quality: Empirical evidence from the UK. Business Strategy and the Environment, 29(6), 2355-2373. https://doi.org/10.1002/bse.2507

Al Shanti, A. M., & Elessa, M. S. (2023). The impact of digital transformation towards blockchain technology application in banks to improve accounting information quality and corporate governance effectiveness. Cogent Economics & Finance, 11(1), 2161773. https://doi.org/10.1080/23322039.2022.2161773

Alassuli, A. (2024). The role of environmental accounting in enhancing corporate social responsibility of industrial companies listed on the Amman Stock Exchange. Uncertain Supply Chain Management, 12(1), 125-132. https://doi.org/10.5267/j.uscm.2023.10.012

Ali, I., Rehman, K., Ali, S., Yousaf, J., & Zia, M. (2010). Corporate social responsibility influences, employee commitment and organizational performance. African journal of business management, 4(12), 2796-2801. https://nachhaltig-sein.info/wp-content/uploads/2012/12/Ali-et-al_CSR-Influences-employee-commitment-and-organizational-performance.pdf

Angotti, M., Ferreira, A. C. D. S., Eugénio, T., & Branco, M. C. (2024). A narrative approach for reporting social and environmental accounting impacts in the mining sector-giving marginalized communities a voice. Meditari Accountancy Research, 32(1), 42-63. https://doi.org/10.1108/MEDAR-11-2021-1513

Appannan, J. S., Mohd Said, R., Ong, T. S., & Senik, R. (2023). Promoting sustainable development through strategies, environmental management accounting and environmental performance. Business Strategy and the Environment, 32(4), 1914-1930. https://doi.org/10.1002/bse.3227

Appiagyei, K., & Donkor, A. (2024). Integrated reporting quality and sustainability performance: does firms' environmental sensitivity matter? Journal of Accounting in Emerging Economies, 14(1), 25-47. https://doi.org/10.1108/JAEE-02-2022-0058

Arif, M., Sajjad, A., Farooq, S., Abrar, M., & Joyo, A. S. (2021). The impact of audit committee attributes on the quality and quantity of environmental, social and governance (ESG) disclosures. Corporate Governance: The International Journal of Business in Society, 21(3), 497-514. https://doi.org/10.1108/CG-06-2020-0243

Asante-Appiah, B. (2020). Does the severity of a client's negative environmental, social and governance reputation affect audit effort and audit quality? Journal of Accounting and Public Policy, 39(3), 106713. https://doi.org/10.1016/j.jaccpubpol.2019.106713

Aziz, A., Salman, S. M., Hassan, M., Younus, M. K., & Uddin, H. F. (2023). The Impact of Audit Firm Size, Auditor Independence and Financial Expertise on Earning Quality: Mediating Role of Audit Quality. Irasd Journal of Economics, 5(4), 1075-1086. https://doi.org/10.52131/joe.2023.0504.0180

Shi, H., Liu, H., & Wu, Y. (2024). Are socially responsible firms responsible to accounting? A meta-analysis of the relationship between corporate social responsibility and earnings management. Journal of Financial Reporting and Accounting, 22(3), 311-332. https://doi.org/10.1108/JFRA-06-2021-0171

دانلود

چاپ شده

ارسال

بازنگری

پذیرش

شماره

نوع مقاله

مجوز

حق نشر 2025 Mona Hashempour Abandansari (Author); Mohammad Mehdi Abbasian Fredoni; Abbas Ali Pour Aghajan, Aliakbar Ramezani, Alireza Modanlo Joibary (Author)

این پروژه تحت مجوز بین المللی Creative Commons Attribution-NonCommercial 4.0 می باشد.