A Model for Operational Budgeting in Fossil Fuel Power Plants Based on Machine Learning and Grounded Theory

Keywords:

operational budgeting, power plants, fossil fuels, machine learning, electricity productionAbstract

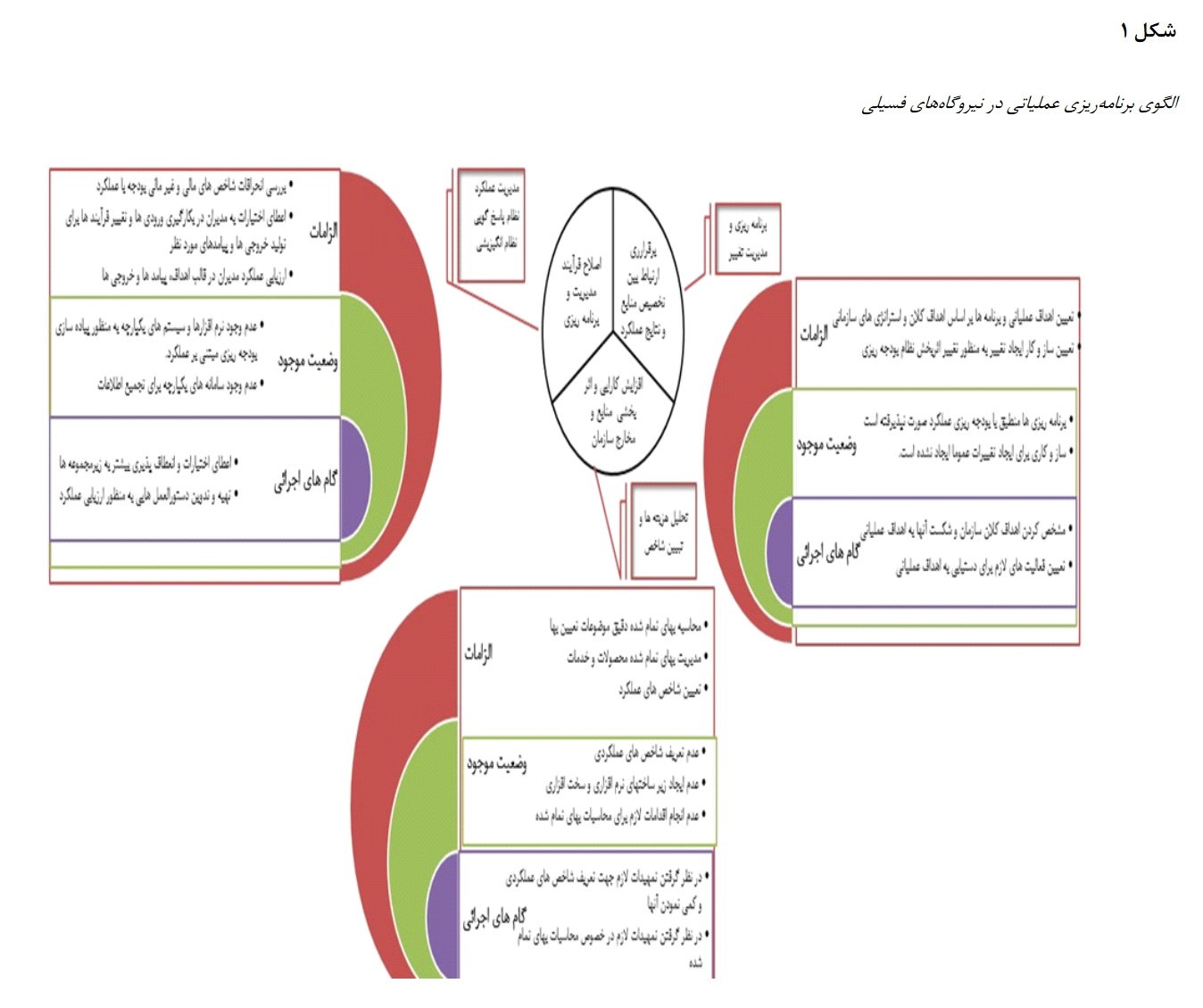

The present study aims to provide a comprehensive model for operational budgeting in fossil fuel power plants based on machine learning and grounded theory. This research examines the impact of a participatory approach to performance-based budgeting on accountability in the public sector. Performance-based budgeting establishes a foundation for greater accountability in the utilization of organizational resources. Additionally, issues such as environmental protection, the high cost of initial investment, and optimal resource utilization play a direct role in the performance of market participants. Unfortunately, in the new competitive conditions, traditional and classical models that assume economic agents (producers or consumers) are homogeneous and lack interaction do not provide the necessary efficiency or satisfactory results. Operational analysis elucidates the behavior of heterogeneous production units and allows for interaction and learning in a dynamic environment. However, due to the model's vast scope and complexities, an analytical solution cannot be used to obtain variables under equilibrium conditions. Considering advances in computational technology, the results of agent-based models can typically be evaluated using simulation methods within various scenarios. Production units submit their proposed production schedules for each hour to the operating entity daily. This entity, based on the forecasted demand for the next twenty-four hours and by implementing an auction mechanism, determines the winning units and market price, followed by executing a settlement mechanism for sales and payments. Given the necessity of balancing consumption and production across the country and the geographical distribution of production and consumer units, the auction mechanism considers not only the consumption amount but also the economic and technical constraints related to production, transmission, and distribution. The research findings indicate that existing performance-based budgeting infrastructures have no effect on financial accountability in the public sector, whereas they have a negative impact on operational accountability. Implementing performance-based budgeting infrastructures and adopting a participatory approach in budgeting enhances the level of governmental accountability in the public sector.

Downloads